If you have never used a pawn loan before, the hardest part is not the counter. It is the uncertainty. People worry they will sign something they do not fully understand, then realize later that the math did not work the way they assumed.

This article is written to remove that uncertainty. It explains pawn shop loans in plain language, breaks down what actually drives the total cost, and gives simple examples you can use to sanity check any ticket in front of you. The goal is not to talk you into a loan. The goal is to make sure you understand the real cost before you agree to anything.

Why people look up costs before taking pawn shop loans

Most borrowers are not rate shopping the way they would for a car loan. They are trying to avoid surprises. The practical question is not, “What is the interest rate,” it is, “What will I have to pay to get my item back, and what happens if I need more time.”

There is also a second concern that comes up often. People want to know whether the shop is going to use confusing language, rush the paperwork, or hide fees in the fine print. That is a valid concern, and it is exactly why a transparency first approach matters.

The real fear, signing something you do not fully understand

When someone searches pawn shop and loans, they are usually in a hurry. A bill is due, a repair cannot wait, or a situation needs cash today. Urgency makes people more likely to accept terms without reading closely. That is where regret starts.

A pawn loan should never feel like a trick. You should be able to ask what the total cost to redeem is, what the due date is, and what changes if you need more time. If those answers are not clear, the loan is not ready to sign.

Why “cheap money” is rarely the point, speed and simplicity usually are

Pawn loans exist because they are simple. They are collateral based, and the decision is tied to the item, not your credit file. That speed is often the advantage. The trade off is that you need to be confident you understand the cost, because the timeline and fees can matter as much as the interest.

What a pawn loan actually is, in plain terms

A pawn loan is a collateral loan. You bring in an item, the shop evaluates it, and the shop offers a loan amount based on what it can reasonably recover if the loan is not redeemed. You receive cash, and the item is held as collateral.

If you repay according to the terms, you get the item back. If you do not, the shop keeps the item, and the debt does not follow you in the way many other loan products do. That structure is the reason loan and pawn options appeal to people who need speed without long paperwork.

Collateral based borrowing vs credit based borrowing

Credit based loans are priced and approved based on your financial profile. Collateral based loans are priced based on the asset in front of the lender. With pawn shop loans, the collateral is the entire risk model.

That also explains why the process feels different. You are not pitching yourself. You are presenting an item.

Where loan and pawn fits in, and who it helps most

A pawn loan can be a reasonable tool when you need short term liquidity and you want the option to get your item back. It is often used for jewelry, watches, tools, and other items with resale value.

It is less suitable when you already know you will not be able to redeem in the timeline. In that case, selling may be cleaner, because it reduces fees and removes the stress of a deadline.

When selling is the cleaner choice, and when it is not

Selling is usually cleaner when the item is not sentimental, or when you are replacing it anyway. Pawning is usually better when the item matters to you, or when it is expensive to replace.

If the item is an engagement ring or a piece of jewelry with personal meaning, it can help to read a decision focused guide before choosing.

The parts of a pawn loan that determine what you pay back

The total cost of a pawn loan is not a mystery if you break it into the parts that create it. These are the components you should understand before you sign.

The loan amount, what it is tied to and what it is not

The loan amount is tied to what the shop believes it can recover through resale if the item is not redeemed, after accounting for costs and risk. It is not tied to the original purchase price, and it is not tied to the highest price you saw online.

If you are borrowing against gold, understanding how value is framed can help you set realistic expectations.

Interest, the number people focus on first

Interest is the cost of borrowing the money over time. People focus on it because it feels like the headline number. But interest does not tell the full story unless you know how it is applied and over what timeline.

The most practical question is not the rate itself. It is how the interest and time combine to create your total redemption amount.

Fees, where people get surprised

Some of the worst pawn experiences are not about the offer. They are about fees that were not understood at signing. You should ask directly whether there are fees beyond interest, when they apply, and whether they change if you extend.

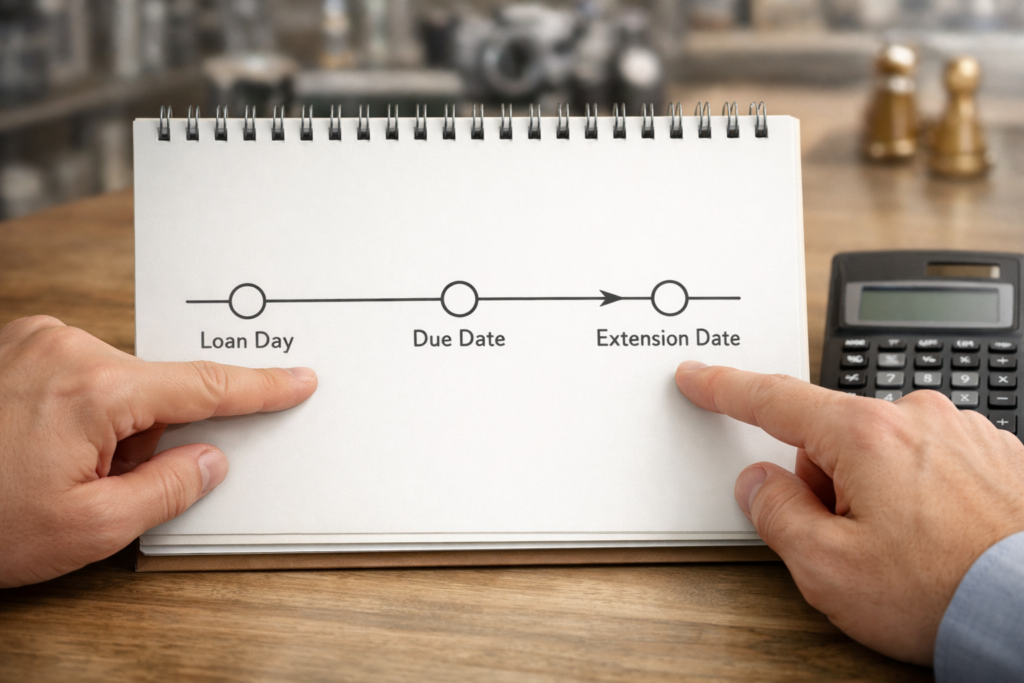

Time, how the calendar changes the total cost

Time matters because costs accumulate over time. A loan that feels manageable in the first weeks can feel heavy if it stretches longer than you planned. Your timeline is often more important than the rate, because it determines how long costs apply.

Pawn shop interest rates in Illinois, what you can and cannot compare

It is tempting to treat pawn loans like other consumer loans, where you compare a single interest rate and pick the lowest. That approach usually fails, because pawn pricing varies by structure and by how shops present the numbers.

What you can compare is the total cost to redeem on a specific date, and how the shop handles extensions. That tells you what the loan will actually cost you.

Why pawn shop and loans are not priced like personal loans

Personal loans are built on credit risk models, underwriting, and long repayment schedules. Pawn loans are built on collateral and shorter timelines. The shop is evaluating the item, holding it, storing it, and taking resale risk.

That does not justify surprises. It simply explains why the pricing structure is different, and why the terms need to be clear.

What varies between shops even inside the same city

Even within the same city, different shops have different evaluation approaches, different inventory needs, and different policies around time. Some explain clearly. Some do not.

When you are considering a pawn shop chicago il option, judge the clarity of the terms as part of the deal.

What to ask so you can compare apples to apples

To compare properly, ask for the total cost to redeem on the due date, ask what happens if you extend, and ask whether any fees apply beyond interest. If the shop cannot answer those questions plainly, you cannot compare it.

Simple cost examples, what a pawn loan really costs in Chicago

These examples are intentionally simple. They are not meant to replace the terms on your ticket. They are meant to show the logic you should use when reading any pawn agreement.

Example 1, small ticket loan with a short timeline

Imagine you take a small pawn loan to cover an immediate expense, and you plan to redeem quickly. The smart move is to confirm the total redemption amount and the due date at signing. If you redeem on time, you should know exactly what you are paying, and why.

The trust test is simple. You should be able to ask, “What is the total cost to redeem on the due date,” and get a clear number.

Example 2, mid range loan where time makes the difference

Now imagine a mid range loan where your plan depends on when you get paid. In this scenario, time becomes the driver. If your paycheck timing shifts, the loan cost changes.

This is where you must understand extension rules in advance. If you may need more time, ask how additional time is calculated and what the new total cost would look like.

Example 3, higher value item with a longer hold

For higher value items, people often assume the terms will be more flexible. Sometimes they are, sometimes they are not. You should still treat it the same way. Confirm the due date, confirm the total redemption amount, and confirm what happens if you need more time.

A high value item can be the most emotionally stressful to lose. If the timeline is uncertain, consider whether selling is cleaner than risking a missed date.

How to read your pawn ticket using the same logic

When you read a pawn ticket, look for four things. The loan amount, the due date, the total cost to redeem on that date, and the terms for additional time. If any of those are unclear, ask before you sign.

The questions to ask before you sign, so there are no surprises

If a shop is truly transparent, these questions should not make anyone uncomfortable. They are the normal questions a borrower should ask.

“What is the total cost to redeem on the due date”

This is the most important question because it collapses the math into a single number. You are not asking for theory. You are asking for your real obligation.

“What happens if I need more time”

Life is messy. If you may need an extension, ask how it works, when it must be requested, and how it changes the total cost.

“Are there any fees beyond interest”

Ask this directly. If the answer is vague, ask for clarification. A clean loan should not rely on hidden fees.

“How do you calculate extensions or additional time”

You do not need a lecture. You need a clear explanation of what changes and how it is applied.

“What exactly happens if I miss the date”

Do not assume. Ask. You should understand the consequences before they happen.

What changes the deal, and what does not

Some factors can affect the loan amount or the shop’s comfort in making an offer. Other factors are noise.

Item category, how jewelry differs from electronics or tools

Jewelry is often easier to price consistently because value can be tied to metal content and condition. Electronics and tools are more dependent on working condition, completeness, and resale demand.

This is one reason different categories can feel like they have different “rules,” even under the same loan structure.

Documentation and condition, when it affects the loan amount

Documentation can reduce uncertainty. For watches, jewelry, and electronics, receipts, boxes, and certificates can support confidence. Condition matters because it affects resale risk.

A shop that takes evaluation seriously will ask smart questions about condition and completeness.

Your payment plan, why your timeline matters more than the rate

If you know exactly when you can redeem, pawn shop loans can be predictable. If your timeline is uncertain, the cost becomes harder to manage. The most responsible approach is to match the loan to a realistic redemption plan.

Common misunderstandings that lead to regret

Most regret comes from assumptions. These are the ones that show up most often.

Thinking the loan works like a payday product

Pawn loans are not the same as a payday product. The structure is different because the collateral changes the risk. But the borrower responsibility is the same. You still need to understand the total cost and the timeline.

Assuming you can extend forever

Some people treat pawn loans like open ended arrangements. That assumption can be expensive. If you need flexibility, confirm it in advance, in writing.

Focusing only on the interest rate and ignoring time and fees

A rate without a timeline tells you almost nothing. The same rate can create very different total costs depending on how long the loan runs and what fees apply.

Not reading the ticket until it is too late

This is the most preventable mistake. Read the ticket while you are still at the counter. If anything is unclear, ask. A reputable shop expects that.

pawn shop chicago il, how to choose a shop based on transparency

The best shop is not the one with the flashiest sign. It is the one that treats the loan like a real financial transaction, with clear explanations and clean paperwork.

The trust checklist, clear terms, readable paperwork, calm explanations

A trustworthy shop explains the total redemption amount, the due date, and extension rules without pressure. The paperwork matches the verbal explanation. You are given time to read and confirm.

If you are evaluating Clark Pawners as your pawn shop chicago il option, use the same checklist. A no surprises approach should be visible in the way the process is handled.

Red flags, vague language, rushed signatures, missing details

If staff rushes you, deflects questions, or cannot explain terms plainly, leave. If paperwork is unclear, do not sign.

Why “no surprises” matters more than a slightly higher offer

A slightly higher loan amount can be tempting. But if the terms are confusing, the risk is higher. Transparency is part of the deal.

pawn shop open near me, what to do when you need cash today

Urgency can cause bad decisions. If you need a pawn shop open near me today, use a fast method that still protects your interests.

A fast short list method for comparing two shops

Pick two shops. Read recent reviews for patterns around clarity and fairness. Call both. Ask what identification is needed, whether evaluation is done in front of you, and whether they can clearly explain total redemption cost and extension rules.

Then choose the shop that sounds calm, clear, and professional.

Timing and safety basics when you are carrying valuables

Go during daylight if possible. Park close. Keep valuables discreet. Do not display jewelry or cash outside. If you feel uncomfortable, do not proceed.

How to protect yourself if you are under pressure

Pressure is a signal. If you feel rushed to sign, stop. Read the ticket. Ask the questions. If you do not get clear answers, walk out. You can always return later.

Next steps, a clean plan to use pawn shop loans responsibly

Pawn loans can be useful when you treat them like a tool, not a last resort. A simple plan keeps them predictable.

Decide your goal, borrow and redeem or sell and move on

If you want the item back, choose a loan and match the timeline to your real budget. If you do not care about keeping the item, selling may be simpler.

Prepare your item and bring what supports value

Bring identification. Bring documentation. Bring accessories, chargers, or boxes when relevant. These details reduce uncertainty and can support a stronger offer.

If you are borrowing against gold, it can help to understand the basics of value and payout expectations.

Confirm terms, total cost, due date, extension rules

Before you sign, confirm the total cost to redeem on the due date, confirm the due date itself, and confirm what happens if you need more time.

Choose the shop that explains clearly and documents everything

A trustworthy shop is not offended by reasonable questions. It answers them plainly and gives you paperwork that matches what you were told.

If you want a no surprises process, choose the place that makes clarity the default.

FAQ

Are pawn shop loans expensive compared to other options?

They can be, depending on how the costs are structured and how long you carry the loan. The most honest way to evaluate the cost is to ask for the total redemption amount on the due date, and what changes if you extend.

What is the single most important number to confirm before signing?

Confirm the total cost to redeem on the due date. That number tells you what the loan will actually cost if you follow the timeline.

Do all pawn shops explain terms the same way?

No. Some are transparent and calm, others are vague or rushed. That is why asking direct questions and reading the ticket before signing matters.

If I miss the due date, do I still owe money?

You need to ask the shop exactly what happens if you miss the date, based on the terms on the ticket. Do not assume. The consequence should be clearly explained before you sign.

Can documentation increase the loan amount?

Sometimes. Documentation and completeness can reduce uncertainty, which can affect the offer, especially for watches, jewelry, and electronics.

When should I sell instead of pawn?

Sell when you do not expect to redeem, or when the item is not sentimental and you want the cleanest outcome. Pawn when you want the option to get it back and your timeline is realistic.

Closing, choose the loan you can actually finish

The best pawn loan is the one you understand completely before you sign. The rate is only one part of the story. Time, fees, and extension rules often matter more.

If you are considering pawn shop loans in Chicago, walk in with a plan. Decide whether you are borrowing to redeem or selling to move on. Bring what supports your item’s value. Ask for the total cost to redeem on the due date, ask what happens if you need more time, and read the ticket while you are still at the counter.

If you want a no surprises experience at Clark Pawners, come in with your item and identification and ask the same transparency questions you would ask anywhere else. A shop that plans to earn your trust should welcome them.